Have you ever wondered why that “free” company perk, like a gym membership or commuter benefit, can sneakily increase your taxable paycheck? In fact, 70% of U.S. workers say they’d consider switching jobs for better compensation ( according to an Economist Impact Study), including non‑cash benefits, and many don’t realize those perks may count as imputed income and impact tax liability.

Understanding imputed earnings isn’t just about compliance. It’s about clarity for HR teams, payroll managers, and finance leaders who need to accurately report and account for these fringe benefits.

In this article, we’ll define imputed income, understand why it matters, and how to handle it correctly, so no one’s caught off guard. So, let’s delve right in.

What is Imputed Income?

Imputed income refers to the value of non-cash benefits an employee receives from an employer that must be counted as taxable income, even though the employee doesn’t receive actual money. These are often fringe benefits like group-term life insurance over $50,000, personal use of a company car, or spouse coverage on health plans.

The IRS requires employers to report and withhold taxes on impute income because it increases an employee’s total compensation. For HR and payroll professionals, accurately identifying and processing imputed earning is critical to stay compliant and avoid tax reporting errors during year-end filings.

Now, that you have a fair idea of imputed income meaning, let’s take a look as what qualifies as imputed taxable income in the next section.

What Are Examples of Imputed Income?

Imputed income arises when an employer provides a non-cash benefit that has a fair market value and is not fully exempt under IRS rules. If you are wondering, “is imputed income taxable?”, here are common imputed earning examples HR, payroll, and finance professionals should watch for:

Adoption Assistance: Employers may reimburse qualified adoption expenses, up to $16,810 in 2024, tax‑free under IRS rules. Employer-paid adoption costs above IRS exclusion limits may be taxable.

Dependent Care Assistance: Benefits over $5,000 annually must be treated as imputed income.

Group Term Life Insurance: GTL Imputed income life coverage exceeding $50,000 is subject to imputed income tax. For instance, a 42-year-old with $250,000 coverage sees around $240/month added as imputed earning.

Gym Membership: If offered for general health (not on-site or job-required), it’s usually taxable.

Relocation Reimbursement: In Q1 2024, 2.4% of U.S. workers moved for new jobs. Non-qualified moving expenses reimbursed by employers are taxable since 2018.

Education Assistance (Under a Threshold): Amounts over $5,250 annually are considered imputed pay.

Personal Use of a Company Car: Any non-business vehicle usage or time logs must be tracked and taxed accordingly.

Employee Discounts: Discounts exceeding IRS limits (20% for services, or cost for goods) are taxable.

Health Insurance for Dependents: If imputed income health insurance covers non-qualified dependents (like imputed income domestic partners), the value may be taxed.

HSA Contributions: Employer HSA contributions are usually exempt, but improper structuring can trigger imputed earning.

Cellphones Provided by the Employer: If used significantly for personal reasons, the value may be taxable.

Housing Provided by the Employer: Unless it meets IRS criteria for being job-required, housing is often taxable.

Retirement Planning Services: If extended beyond basic financial education, services may be taxable.

Company Trips: Team building activities like vacations or incentive trips not related to business duties can be considered taxable income.

Recognizing these examples ensures accurate payroll reporting and avoids compliance issues with the IRS. Being proactive also helps employees understand the true value, and tax implications of their compensation packages.

What is Excluded from Imputed Income?

While many fringe benefits are taxable, the IRS also defines several benefits that are excluded from imputed income, meaning they are not subject to federal income tax when certain conditions are met.

Knowing these exclusions helps employers stay compliant and avoid unnecessary tax withholdings.

Health Insurance for Qualified Dependents: Coverage for legal spouses and dependent children is not considered imputed earning.

Group-Term Life Insurance (Up to $50,000): The first $50,000 of employer-provided coverage is exempt from imputed income GTL taxation.

De Minimis Fringe Benefits: Occasional, low-value items like coffee, snacks, or holiday gifts (excluding cash/gift cards) are typically tax-free.

Qualified Employee Discounts: Discounts within IRS limits, such as up to 20% on services or below cost on merchandise are exempt.

Working Condition Fringe Benefits: Items used for business purposes, like work laptops or phones, are excluded if their use is primarily job-related.

On-Premises Meals: Meals provided on-site for the employer’s convenience may be tax-exempt under specific conditions.

Qualified Transportation Benefits: Transit passes and parking up to IRS limits (e.g., $315/month in 2025) are usually not taxable.

No-Additional-Cost Services: If an employee receives services (like airline flights or hotel stays) that cost the employer nothing extra, they’re not considered income.

Education Assistance (Up to $5,250/year): Employer-paid tuition or education costs under this amount for career growth can be tax-free.

Retirement Contributions: Employer contributions to qualified retirement plans like 401(k)s are not taxable until withdrawn.

Understanding what is excluded from imputed pay ensures accurate payroll reporting and enhances employee satisfaction. HR and payroll teams should regularly review IRS guidelines and communicate clearly with staff about which benefits affect take-home pay, and which don’t.

How is Imputed Income Calculated?

Imputed income is calculated by determining the fair market value (FMV) of a non-cash benefit provided to an employee, then subtracting any amount the employee contributes toward that benefit. The result is the taxable value that must be included in the employee’s gross income for tax reporting purposes.

An imputed income calculator can come in handy here.

Basic Formula

Imputed Income = Fair Market Value (FMV) – Employee Contributions (if any)

Here are a few examples to illustrate:

Example 1: Group-Term Life Insurance

Let’s say your company provides $100,000 in group-term life insurance coverage. The first $50,000 is tax-exempt. To calculate imputed income life insurance for the excess:

IRS Table I is used to determine the monthly cost based on age.

For a 40-year-old, the IRS cost is $0.10 per $1,000 per month.

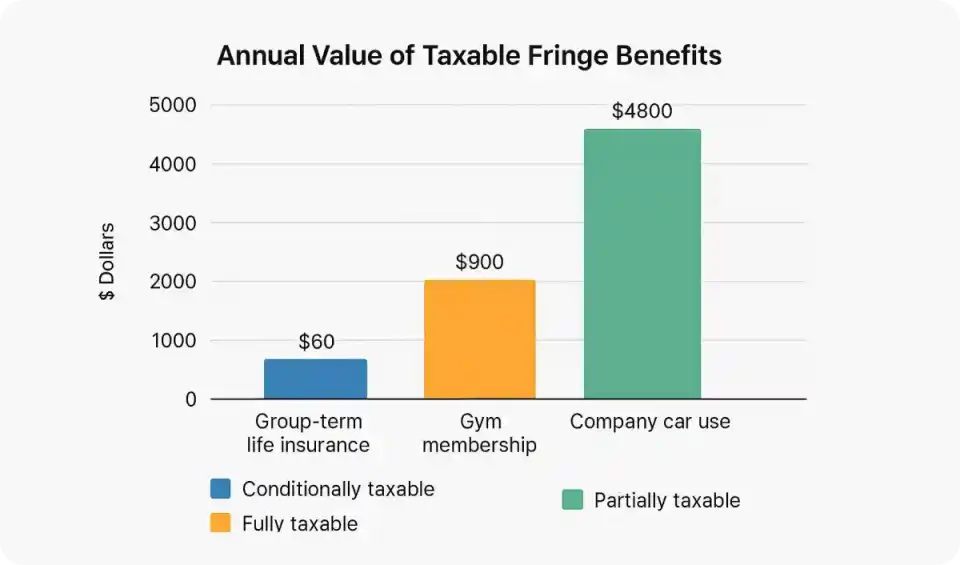

If the FMV of a car benefit is $500/month and the employee pays $100 toward its use:

Imputed Income = $500 – $100 = $400/month

Annual Imputed Income = $400 × 12 = $4,800

Example 3: Gym Membership

An employer pays $900/year for a commercial gym membership. If the employee pays nothing:

Imputed Income = $900 – $0 = $900

HR and payroll teams must ensure accurate valuation using IRS-approved methods and documentation. Failing to calculate imputed pay correctly can result in W-2 reporting errors, underwithheld taxes, or IRS penalties, especially during audits. Regular reviews of fringe benefit policies can help keep calculations compliant and consistent.

How is Imputed Income Taxed?

Imputed income is taxed just like regular wages. It’s added to an employee’s gross income and subject to federal income tax, Social Security, Medicare, and in many cases, state and local income taxes. Although the employee doesn’t receive this income in cash, it still increases their taxable earnings, which impacts their paycheck and W-2.

How It Works?

Once imputed pay is calculated (based on fair market value minus any employee contributions), it’s added to the employee’s payroll record. Employers must then withhold:

Federal Income Tax (FIT)

Social Security Tax (6.2%)

Medicare Tax (1.45%)

State and Local Taxes (where applicable)

Note: Imputed earning is not subject to federal unemployment tax (FUTA).

Example 1: Group-Term Life Insurance

Let’s say an employee has $60 in annual imputed GTL income from excess life insurance coverage.

Assuming a 22% federal tax rate:

FIT = $60 × 0.22 = $13.20

Social Security = $60 × 0.062 = $3.72

Medicare = $60 × 0.0145 = $0.87

Total Imputed Income Tax Withheld = $17.79

Example 2: Company Paid Gym Membership

Annual value = $900

No employee contribution

Taxed as part of wages

Assuming a 24% federal tax rate:

FIT = $216

Social Security = $55.80

Medicare = $13.05

Total Imputed Income Tax = $284.85

These taxes are typically withheld from the employee’s paycheck over the year or included as a lump sum during bonus or final payroll runs. Employers must report total imputed pay on Box 1 of Form W-2 and applicable amounts in Boxes 3 and 5 for Social Security and Medicare.

Proper handling ensures tax compliance and prevents underreporting that could lead to IRS penalties.

How Does Imputed Income Affect Your Taxes?

Imputed income can increase your taxable wages, even though you don’t receive extra cash. This means you’ll likely owe more in income taxes and may see a smaller net paycheck, especially if your employer withholds the tax in a lump sum at year-end.

For employees, understanding how imputed earning affects your taxes helps avoid surprises during tax season.

Here’s How It Impacts You:

Higher Taxable Income: Imputed earning is added to your gross pay, increasing your total income on Form W-2 (Box 1).

More Payroll Taxes: It’s also subject to Social Security and Medicare (Boxes 3 and 5), meaning higher payroll tax deductions.

Possibly Higher Tax Bracket: If your total income pushes you into the next tax bracket, you may owe a higher percentage of tax overall.

No Extra Cash Received: Since you’re being taxed on a benefit you didn’t receive as cash, the actual paycheck won’t reflect this increase, making it feel like a “phantom tax.”

Real-Life Example:

Let’s say your company gives you a $1,200/year gym membership. You didn’t pay for it, but the IRS sees it as income. If you’re in the 22% federal tax bracket, here’s what happens:

Federal Tax Owed: $1,200 × 22% = $264

Social Security Tax: $1,200 × 6.2% = $74.40

Medicare Tax: $1,200 × 1.45% = $17.40

Total Tax Impact = $355.80/year

For HR and payroll teams, it’s essential to clearly communicate these impacts during open enrollment and year-end to help employees plan ahead. For employees, reviewing imputed income on paystubs and W-2s entries can prevent underpayment issues when filing your annual return.

How Do Employers Report Imputed Income?

Employers are required to track, calculate, and report imputed income accurately to ensure compliance with IRS regulations. Even though the employee doesn’t receive cash, imputed earnings must be treated as taxable wages and included in the employee’s annual Form W-2.

Key Reporting Steps:

Identify Taxable Fringe Benefits: HR and payroll must determine which non-cash benefits, like life insurance, personal use of a company car, or dependent health coverage, qualify as imputed taxable income.

Calculate Fair Market Value (FMV): Use IRS-approved methods to calculate the FMV of each benefit and subtract any employee contributions to determine the taxable portion.

Update Payroll Records: Impute income should be added to the employee’s gross wages in payroll, even if it’s not paid in cash. This ensures accurate tax withholding throughout the year.

Withhold Applicable Taxes: Employers must withhold federal income tax, Social Security, and Medicare, and sometimes state/local taxes on imputed earning. These withholdings can be spread throughout the year or withheld in a single payroll cycle.

Report on Form W-2: Form W-2 consists of three boxes namely:

Box 1: Includes total wages, tips, and other compensation (including imputed earning).

Box 3 & 5: Include Social Security and Medicare wages if applicable.

Box 12: Certain imputed earning types, like group-term life insurance over $50,000, must be listed with Code “C.”

Communicate with Employees: Provide explanations of imputed income items on year-end pay statements or in benefits summaries to avoid confusion.

Properly reporting imputed income not only ensures IRS compliance but also helps employees understand their total compensation and tax responsibilities. Errors in reporting can lead to penalties, amended returns, and employee dissatisfaction, making accurate tracking and documentation essential for every employer.

What Happens If Imputed Income is Not Reported?

Failing to report imputed income correctly can lead to serious tax and compliance consequences for both employers and employees. Since imputed pay increases an employee’s taxable wages, omitting it can distort payroll records, understate tax liabilities, and trigger IRS scrutiny.

Consequences for Employers

IRS Penalties & Fines: The IRS may impose penalties for inaccurate W-2 filings, underreported wages, and failure to withhold proper taxes (federal, Social Security, Medicare).

Back Taxes & Interest: If imputed income is discovered during an audit, the employer may owe back taxes plus interest and penalties on the unreported amount.

Compliance Violations: Not reporting imputed pay violates federal and often state payroll compliance laws, risking reputational damage and additional fines.

W-2 Corrections: Employers may be required to issue corrected W-2s (Form W-2c), creating administrative burdens and frustrating employees.

Consequences for Employees

Underpayment of Taxes: Employees may unknowingly underpay their taxes, resulting in unexpected tax bills or penalties during tax filing season.

Amended Returns: If the error is caught after filing, employees may need to submit amended tax returns, leading to delays and possible fees.

Audit Risk: Missing or inaccurate income records can raise red flags with the IRS, increasing the chance of audits or compliance reviews.

Imputed income reporting is not optional. It’s a critical part of accurate payroll and tax reporting. Employers must implement processes to track fringe benefits, calculate their imputed income taxable value, and ensure everything is reported correctly on employee W-2s.

Staying ahead of imputed pay responsibilities protects both your business and your workforce from costly tax consequences.

Imputed Income vs Taxable Income vs Fringe Benefits

Understanding the difference between imputed income, taxable income, and fringe benefits is crucial for accurate payroll processing, compliance, and financial reporting.

The table below breaks down how these three terms differ, and how they often overlap.

Category

Imputed Income

Taxable Income

Fringe Benefits

Definition

Non-cash benefits provided by employers that are treated as income for tax purposes

Total income subject to tax, including wages, bonuses, and imputed income

Perks or benefits offered to employees in addition to regular wages

Cash Received?

No direct cash received

Yes, generally includes direct payments

Often non-cash (e.g., insurance, company car, gym membership)

Examples

Personal use of company car, domestic partner health coverage

Salary, bonuses, commissions, tips

Health insurance, tuition assistance, relocation, meals, wellness programs

Reported on W-2?

Yes, included in Box 1 (and Box 12 with applicable codes)

Yes, reported in various boxes depending on type

Some are reported (if taxable), others are not (if excluded by IRS)

Tax Withholding?

Subject to FIT, Social Security, and Medicare taxes

Full tax withholding applies

Depends: taxable benefits are withheld; non-taxable are excluded

IRS Guidance?

IRC Section 61 and fringe benefit valuation rules

IRC Section 61, 3401, and other income tax regulations

IRS Publication 15-B defines which benefits are taxable or excluded

Impact on Employees

Increases taxable wages without increasing take-home pay

Directly affects paycheck and annual tax filing

Enhances total compensation but may have tax implications

Payroll Relevance

Must be added manually or through system config for proper reporting

Calculated automatically from earnings

Requires tracking to determine taxability

This comparison helps HR, payroll, and finance professionals ensure clear, compliant compensation reporting.

Track and Manage Imputed Income Effortlessly with Clockdiary

Clockdiary free timesheet app goes beyond AI-powered time tracking. Its robust payroll and expense features can significantly simplify imputed income management:

Expense Tracking & Receipt Uploads: Log expenses for fringe benefits (e.g., gym memberships, relocation costs) and attach receipts directly to entries, thereby ensuring accurate valuation of taxable benefits.

Customizable Reports & Exports: Generate detailed reports by user, project, or expense type. Export to CSV, Excel, or PDF for seamless integration into payroll systems and IRS forms.

Hourly Rates & Cost Tracking: Assign billable and non‑billable rates per employee or project. Helps quantify the cost of personal benefit usage, like company car time, as a monetary value.

Timesheet Approvals & Auditability: Require employees or managers to approve entries related to fringe benefits or reimbursable items. Ensures a clear audit trail and prevents missing or inflated benefit valuation.

Time-Off Policies and Attendance Records: Monitor benefit eligibility periods like education assistance or relocation reimbursements tied to tenure or leave. Policies and accurate time-off tracking help verify eligibility.

Integration with Payroll Systems: Export work hours, expense, and benefit reports directly into QuickBooks and ADP, making it easier to incorporate imputed earning into payroll run.

Transparent Dashboards & Ease of Use: Visual dashboards show time and expense distributions across benefit categories, thus helping finance and compliance teams oversee imputed income trends.

By leveraging these capabilities, Clockdiary helps HR and finance teams accurately capture, validate, and report the taxable value of fringe benefits, thereby turning a tedious compliance task into a streamlined, transparent process. Get in touch with us to make this supremely engineered time tracking app an integral part of your workplace and you will be good to go.

Common FAQs About Imputed Income

What Does Imputed Income Mean?

Imputed income means the taxable value of non-cash benefits an employee receives from their employer, such as personal use of a company car or life insurance over $50,000. Even though no money is paid directly, the IRS requires this value to be included in the employee’s gross income for tax purposes.

What Are Imputed Earnings?

Imputed earnings refer to non-cash compensation or benefits assigned a monetary value and treated as taxable income, even though the employee doesn’t receive them directly in wages. Common examples include personal use of company property, excess life insurance coverage, or certain dependent benefits.

How Much Tax Will I Pay on Imputed Income?

The tax you’ll pay on imputed income depends on your federal income tax bracket plus Social Security (6.2%) and Medicare (1.45%) rates. For example, if you’re in the 22% bracket, your imputed income tax rate could be around 29.65% of its value.

Why is Imputed Income Deducted from Your Paycheck?

Imputed income isn’t actually deducted from your paycheck. Instead, it’s added to your taxable wages, which can increase the amount of taxes withheld. This may reduce your net pay because more is taken out for income tax, Social Security, and Medicare based on the higher reported income.

Should I Avoid Imputed Income?

You don’t necessarily need to avoid imputed income. It often comes from valuable perks like health coverage or tuition assistance that enhance your total compensation. However, it’s important to understand the tax impact so you can plan accordingly and avoid surprises at tax time.

Is Imputed Income Considered Compensation?

Yes, imputed income is considered part of an employee’s total compensation because it represents the taxable value of non-cash benefits received. While it doesn’t increase take-home pay, it does increase gross income for tax and reporting purposes.

Is Imputed Income Good or Bad?

Imputed income isn’t inherently good or bad. It simply reflects the taxable value of valuable non-cash benefits like life insurance, company perks, or dependent coverage. While it can slightly increase your tax bill, it often means you’re receiving greater total compensation than just your salary.